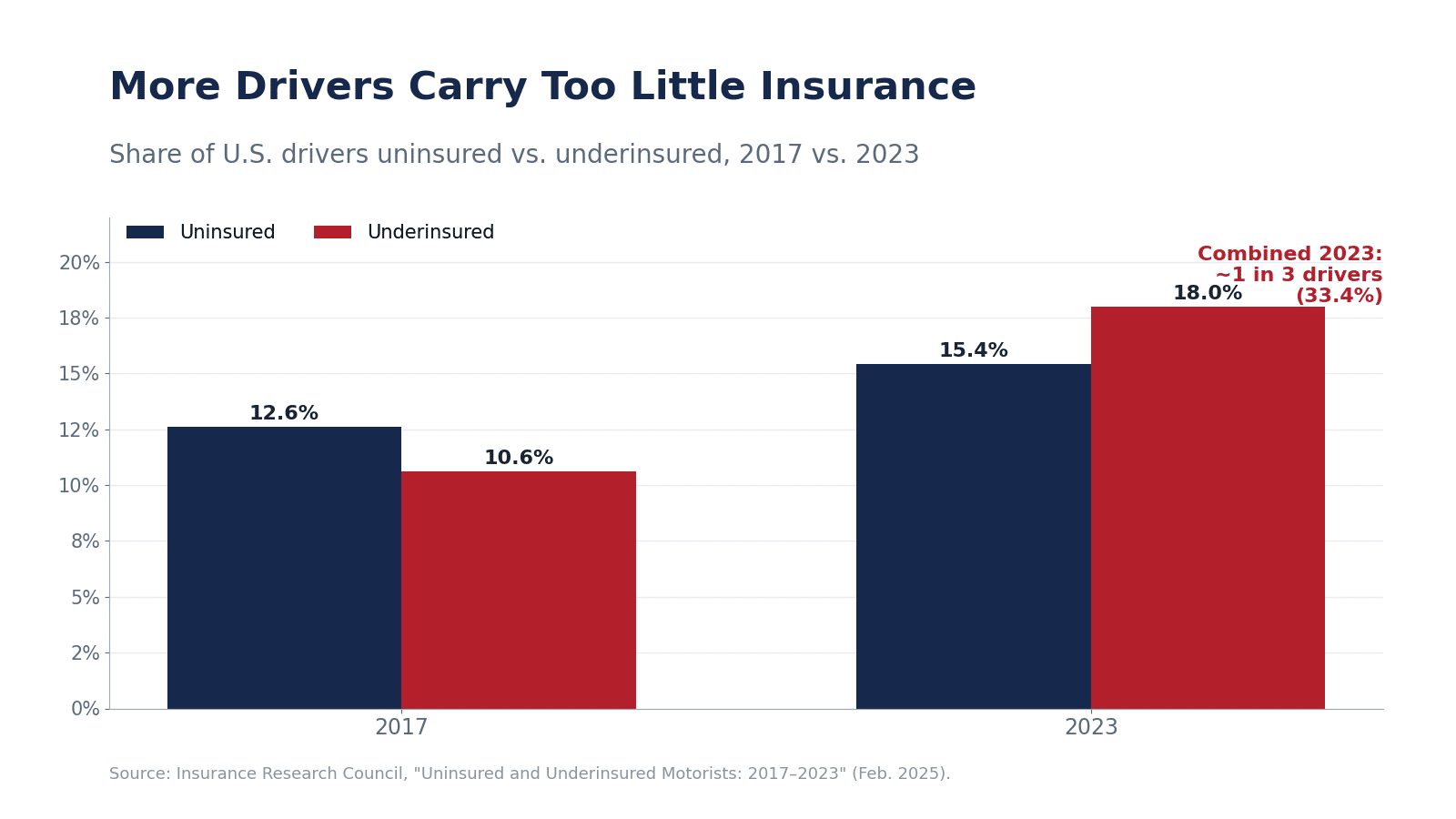

Quick answer: Uninsured/underinsured motorist (UM/UIM) coverage is part of your own auto policy that pays your injury losses when the at-fault driver has no insurance, too little insurance, or flees the scene. In Houston it matters because Texas only requires drivers to carry 30/60/25 minimum limits, and roughly one in three U.S. drivers is uninsured or underinsured. A UM/UIM claim is filed against your own insurer, and Texas law gives it a four-year contract deadline (Tex. Civ. Prac. & Rem. Code § 16.004) — but notify your insurer fast. Call our Houston uninsured motorist lawyers at 346-299-8430 for a free consultation. No fee unless we win.

- UM/UIM is first-party coverage — it pays from your policy, not the at-fault driver’s.

- It covers three situations: an uninsured driver, an underinsured driver whose limits run out, and a hit-and-run that struck you.

- Under Brainard v. Trinity Universal, your insurer owes nothing on a UIM claim until fault and underinsurance are legally established — so we often must file suit.

- The UM/UIM claim is a contract claim with a four-year deadline, but your policy’s notice terms can cut that short — act quickly.

- Texas bars recovery only if you were more than 50% at fault; otherwise your award is reduced by your share.

Houston Uninsured Motorist Claims at a Glance

| Question | Short answer |

|---|---|

| Whose insurance pays? | Your own UM/UIM coverage — a first-party claim |

| Does it cover a hit-and-run? | Yes, if the vehicle physically struck you (Tex. Ins. Code § 1952.104) |

| Deadline to file? | UM/UIM is a 4-year contract claim (§ 16.004) — but give notice and act within 2 years to be safe |

| Do I have to sue my own insurer? | Often yes — Brainard requires a judgment establishing fault and underinsurance |

| Can I recover if partly at fault? | Yes, unless you were more than 50% at fault (§ 33.001) |

| Cost to hire us? | $0 up front — no fee unless we win |

| Where are you located? | 340 N Sam Houston Pkwy E, Ste A1045, Houston, TX 77060 |

Sources: Insurance Research Council, “Uninsured and Underinsured Motorists: 2017–2023” (Feb. 2025); Tex. Civ. Prac. & Rem. Code § 16.004.

What Is Uninsured/Underinsured Motorist Coverage in Texas?

Uninsured/underinsured motorist coverage is a part of your own Texas auto policy that steps into the shoes of an at-fault driver who cannot pay. It pays your bodily-injury losses — and, with the property-damage option, your vehicle damage — in three situations: the other driver had no insurance, the other driver had insurance but not enough to cover your injuries, or the other driver was a hit-and-run who struck your car. Texas insurers must offer UM/UIM coverage on every auto policy, and you only go without it if you rejected it in writing (Tex. Ins. Code § 1952.101). Because it is first-party coverage, you pursue it against your own insurance company rather than the other driver — which is exactly why these claims have rules of their own.

Does Uninsured Motorist Coverage Cover a Hit-and-Run in Houston?

Yes. Under Texas law a hit-and-run driver is treated as an uninsured motorist, so your UM coverage can pay for a fleeing driver who hurt you. There is one important catch for an unidentified “phantom” vehicle: Texas requires actual physical contact between the hit-and-run vehicle and you or your car (Tex. Ins. Code § 1952.104). A true “miss-and-run” — where a car forced you off the road but never touched you — is generally not covered unless your policy specifically adds it. Either way, call the police and report the crash immediately: a prompt police report is often the evidence that proves another vehicle was involved.

What If the At-Fault Driver Was Underinsured?

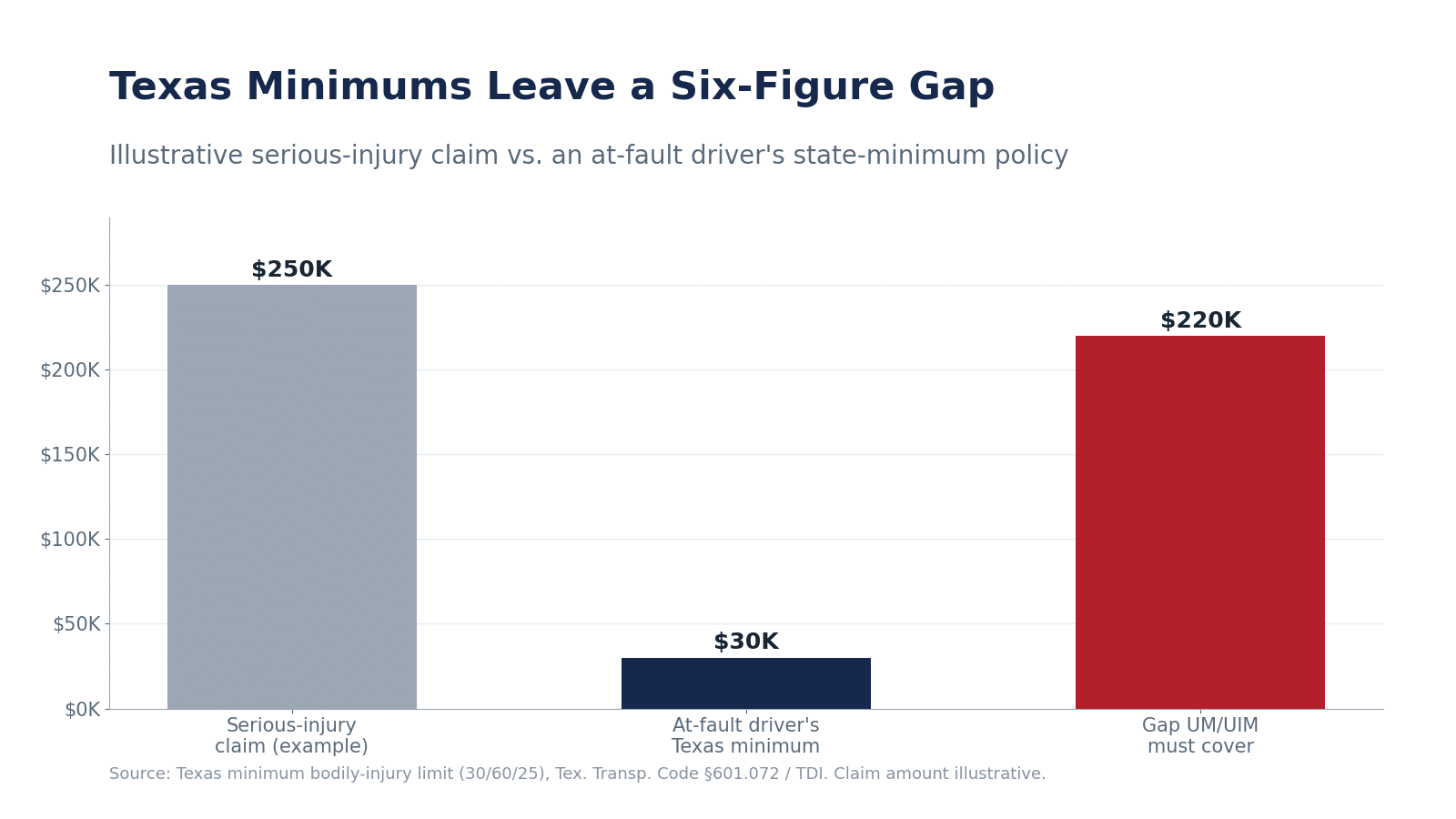

This is the most common — and most overlooked — situation. Texas only requires drivers to carry minimum liability limits of 30/60/25: $30,000 per injured person, $60,000 per crash, and $25,000 in property damage. When a serious crash leaves you with surgery, lost income, and long-term care, a $30,000 minimum policy disappears almost instantly. Underinsured motorist coverage fills that gap, paying the difference between what the at-fault driver’s policy covers and what your injuries are actually worth, up to your own UIM limit.

Do I Have to Sue My Own Insurance Company?

Often, yes — and it is nothing personal; it is how the Texas UM/UIM system is built. In Brainard v. Trinity Universal Insurance Co., 216 S.W.3d 809 (Tex. 2006), the Texas Supreme Court held that an underinsured-motorist insurer owes nothing until the insured obtains a judgment establishing the other driver’s liability and underinsured status. In plain terms, your insurer can sit back until a court (or a binding agreement) fixes who was at fault and how much your damages are. That is why we frequently file suit to establish those facts — and the Texas Supreme Court has confirmed you may bring a declaratory-judgment action against your own carrier to do exactly that (In re Farmers Texas County Mutual Insurance Co., 621 S.W.3d 261 (Tex. 2021)). Texas even sets where that suit is filed: a UM/UIM action must be brought in the county where you lived at the time of the crash (Tex. Ins. Code § 1952.110) — for our Houston clients, that is typically the Harris County district courts, with some disputes heard in the U.S. District Court for the Southern District of Texas, Houston Division.

Your insurer is not your friend in a UM/UIM claim. The same company you pay premiums to becomes the party trying to pay you as little as possible. Having your own lawyer levels the field.

Will My Insurance Rates Go Up If I File a UM/UIM Claim?

Filing a UM/UIM claim means using coverage you already paid for after a crash you did not cause. You were not the at-fault driver — the uninsured or underinsured driver was. Texas insurers generally cannot surcharge or refuse to renew you because of a not-at-fault claim, and many drivers are surprised to learn the coverage they hesitate to use is the very coverage they bought for this exact moment. Every policy and carrier is different, so we are glad to review yours and explain what to expect before you file.

How Long Do I Have to File a UM/UIM Claim in Texas?

This is where UM/UIM claims get tricky. Because the claim is a contract claim against your own insurer, the Texas breach-of-contract deadline of four years applies (Tex. Civ. Prac. & Rem. Code § 16.004) — longer than the two-year deadline for suing the at-fault driver directly (§ 16.003). But do not count on the full four years. Your own policy almost always requires prompt notice of the crash and your cooperation, and a missed notice or policy limitation provision can bar your claim long before four years pass. Because the underlying crash facts still have to be proven, the safest course is to treat the two-year tort clock as your working deadline and contact us right away.

What Is My Houston UM/UIM Claim Worth?

Your claim is worth your full damages — medical bills, future care, lost income and earning capacity, and pain and suffering — up to your UM/UIM limits, after crediting whatever the at-fault driver’s insurer pays. Two Texas rules shape the number. First, your insurer gets a credit (offset) for the amount recovered from the at-fault driver, so UIM pays the gap above it. Second, Texas generally does not allow “stacking” of UM/UIM limits from separate policies to multiply your recovery. We document the full value of your injuries — and push past the insurer’s lowball valuation — so the policy limits you paid for are not left on the table.

What If I Was Partly at Fault for the Crash?

You can still recover, as long as you were not mostly to blame. Texas uses proportionate responsibility (Tex. Civ. Prac. & Rem. Code § 33.001): you are barred only if you were more than 50% at fault, and otherwise your recovery is reduced by your percentage of fault. Because a UM/UIM claim turns on proving the other driver’s fault, insurers often try to shift blame onto you to shrink what they owe. We build the case with the crash evidence to keep your share of fault from being overstated.

Our Results in Serious Injury Cases

Southern Injury Attorneys has recovered six-figure settlements in serious injury cases, including multiple six-figure results for clients harmed by others’ negligence and a $175,000 recovery in a vehicle-fire case. Every case is different, and these results reflect specific facts and injuries.

Prior results do not guarantee or predict a similar outcome in any future case.

Why Houston UM/UIM Victims Choose Southern Injury Attorneys

Uninsured and underinsured motorist claims are won by lawyers who know the Brainard rules cold, document the full value of your injuries, and are ready to file suit against an insurer that refuses to pay fairly. You work directly with attorneys, and you pay nothing unless we win. We also handle the rest of your case — from the Houston car accident or rear-end collision claim to a truck accident or wrongful death matter — and you can learn more about this coverage on our broad uninsured motorist accident lawyer page.

Houston office: 340 N Sam Houston Parkway E, Suite A1045, Houston, TX 77060

Phone: 346-299-8430 · 800-224-5546

Serving Harris County and the greater Houston metro area. Our firm is headquartered in Memphis and represents injured clients across Tennessee, Mississippi, Arkansas, Texas, Kentucky, and Georgia.

No fee unless we win. The consultation is free, and we advance the costs of investigating your case.

Houston Uninsured Motorist FAQs

What is uninsured/underinsured motorist coverage in Texas?

It is a part of your own auto policy that pays your injury losses when the at-fault driver has no insurance, too little insurance, or fled the scene. Texas insurers must offer it, and you only go without it if you rejected the coverage in writing.

Does uninsured motorist coverage cover a hit-and-run in Texas?

Yes. A hit-and-run driver is treated as uninsured, so your UM coverage can apply. For an unidentified vehicle, Texas requires actual physical contact between the hit-and-run vehicle and you or your car, and you should report the crash to police right away.

Do I have to sue my own insurance company for a UIM claim?

Often yes. Under Brainard v. Trinity Universal Insurance Co., your insurer owes nothing on a UIM claim until a judgment establishes the other driver’s fault and underinsured status, so we frequently file suit — including a declaratory-judgment action against your own carrier — to establish those facts.

Will my insurance rates go up if I use my UM/UIM coverage?

You are using coverage you already paid for after a crash you did not cause. Texas insurers generally cannot surcharge or refuse to renew you for a not-at-fault claim. Every policy is different, so we are glad to review yours before you file.

How long do I have to file a UM/UIM claim in Texas?

A UM/UIM claim is a contract claim with a four-year deadline under Tex. Civ. Prac. & Rem. Code § 16.004. But your policy usually requires prompt notice, and the two-year deadline applies to suing the at-fault driver, so it is safest to act within two years and notify your insurer immediately.

What if the at-fault driver had insurance but not enough?

That is an underinsured-motorist claim. After you exhaust the at-fault driver’s limits, your UIM coverage pays the difference between that amount and your full damages, up to your UIM limit. Texas only requires 30/60/25 minimum limits, so serious injuries often exceed them.

Can I recover UM/UIM benefits if I was partly at fault?

Yes, unless you were more than 50% at fault. Under Texas’s proportionate responsibility rule, your recovery is reduced by your percentage of fault and barred only if you were more than half responsible for the crash.

Can I stack UM/UIM coverage from more than one policy in Texas?

Generally no. Texas does not allow stacking of UM/UIM limits across separate policies in most situations, and your insurer receives a credit for what the at-fault driver pays. The exact result depends on your policy language, which we can review.

How much does it cost to hire a Houston uninsured motorist lawyer?

Nothing up front. We work on contingency, so you pay no attorney fee unless we recover money for you, and the initial consultation is free.

Hit by an uninsured or underinsured driver in Houston? Talk with a UM/UIM lawyer today. Call 346-299-8430 or 800-224-5546, or reach us through our contact page for a free, no-obligation consultation. You pay no fee unless we win.

This page is legal information, not legal advice, and does not create an attorney-client relationship. Outcomes depend on the specific facts of each case. For advice about your situation, speak with a licensed attorney.